Homeowners Insurance Comparison Guide

Choosing the right homeowners insurance policy protects your most valuable investment. Utah homeowners face unique risks from natural disasters, varying construction costs, and local market conditions.

We at Archibald Insurance Agency help property owners navigate the homeowners insurance comparison process. This guide breaks down coverage types, rate factors, and comparison strategies to help you make informed decisions.

What Coverage Do You Actually Need?

Structure Protection Forms Your Foundation

Dwelling coverage protects the physical structure of your home, including walls, roof, foundation, and attached structures like garages. Utah homeowners need adequate dwelling coverage because construction costs rose 40% between 2019 and 2024.

Most insurers require coverage equal to the replacement cost of your home, not its market value. The average home cost in Utah reaches approximately $518,000, which impacts insurance premiums due to higher dwelling limits needed. State Farm offers automatic inflation adjustments to help keep pace with construction costs, while Chubb provides extended replacement cost coverage that goes beyond policy limits.

Personal Property Coverage Protects Your Belongings

Personal property coverage protects your belongings inside the home, typically covering 50-70% of your dwelling coverage amount. Replacement cost coverage pays for new items of similar quality, while actual cash value considers depreciation.

Wind and hail damage affects 2.8 percent of insured homes in a five-year period, which makes adequate personal property limits essential. USAA offers specialized coverage for military uniforms, while Amica provides electronic coverage for modern technology needs.

Liability Coverage Shields You From Lawsuits

Liability coverage protects against lawsuits from accidents on your property, with most policies starting at $100,000. However, homeowners with significant assets should consider umbrella insurance to increase liability protection beyond standard limits.

This coverage becomes particularly important when you consider that medical costs and legal fees can quickly exceed basic policy limits. Understanding how these three coverage types work together helps you evaluate quotes more effectively when you compare different insurance carriers and their rate structures.

What Drives Your Insurance Costs Up or Down

Your location determines the biggest portion of your homeowners insurance premium. Utah homeowners pay an average of $894 annually, which sits below the national average. Salt Lake City residents face higher costs compared to St. George, which reflects different risk profiles across the state. The most expensive areas correlate directly with wildfire zones, earthquake fault lines, and flood-prone regions where insurers face higher claim frequencies.

Natural Disasters Shape Premium Calculations

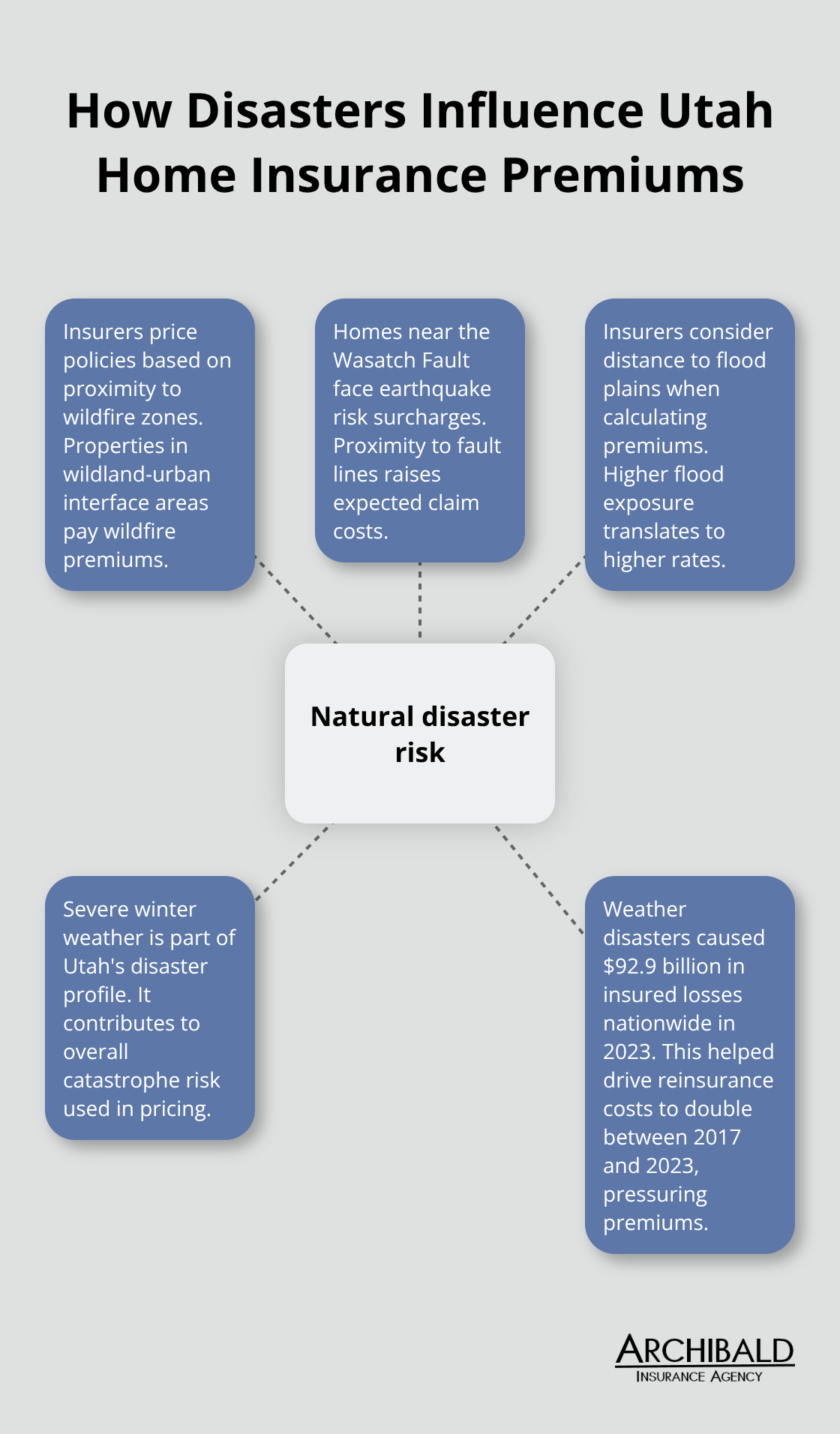

Utah’s natural disaster profile includes wildfires, earthquakes, floods, and severe winter weather. Weather disasters caused $92.9 billion in insured losses nationwide in 2023, which drove up reinsurance costs that doubled between 2017 and 2023. Insurers price policies based on proximity to wildfire zones, earthquake fault lines, and flood plains. Homes near the Wasatch Fault face earthquake risk surcharges, while properties in wildland-urban interface areas pay wildfire premiums.

Home Characteristics Control Rate Variations

Construction materials directly impact your rates. Brick and stone homes cost less to insure than wood frame structures due to fire resistance. Homes built before 1980 face higher premiums because older electrical systems, plumbing, and roofs create increased claim risks. Impact-resistant roofs can reduce premiums between 2-35% (depending on your insurer), while security systems and monitored fire alarms generate additional discounts.

Credit Scores Create Dramatic Price Differences

Utah homeowners with poor credit pay significantly more annually compared to good credit holders, which represents a substantial increase according to industry data. Insurance companies use credit-based insurance scores to predict claim likelihood, which makes credit improvement a direct path to lower premiums. Claims history affects rates for three to five years, with multiple claims potentially leading to non-renewal rather than just rate increases.

These rate factors work together to create your final premium, but you can control many of these variables through smart choices. The next step involves comparing quotes from multiple carriers to find the best combination of coverage and price for your specific situation.

How Do You Compare Insurance Quotes Effectively

Smart quote comparison starts with quotes from at least three different carriers within the same week, since rates change frequently. State Farm offers the cheapest homeowners insurance in Utah at $1,250 annually, while USAA provides military families coverage around $1,300 per year. Chubb commands premium rates but includes complimentary wildfire defense services and extended replacement cost coverage. Request quotes with identical coverage limits and deductibles to make accurate comparisons, then focus on the total annual premium rather than monthly payments that can hide fees.

Match Coverage Limits Across All Quotes

Set your dwelling coverage at your home’s full replacement cost, not market value, since construction costs have increased significantly in recent years. Personal property limits should reflect your actual possessions value, with replacement cost coverage worth the extra premium over actual cash value policies. Liability coverage starts at $100,000, but homeowners with assets that exceed $500,000 need umbrella policies for adequate protection. Deductible choices directly impact premiums – you can reduce costs by double-digit percentages when you raise your deductible from $500 to $1,000.

Examine Policy Exclusions and Special Features

Standard policies exclude earthquake and flood damage, which forces Utah homeowners to purchase separate coverage or endorsements. Amica offers exceptional customer service with low complaint rates, while Auto-Owners charges significantly more at $3,587 annually for comparable coverage. Review each carrier’s claims process, financial stability ratings, and available discounts for security systems or policy bundles. Travelers Insurance averages $1,160 annually and provides competitive rates, but verify their coverage exclusions match your risk tolerance before you make decisions.

Request Detailed Quote Breakdowns

Ask each insurer to itemize their quote components so you can identify where price differences occur. Some carriers charge separate fees for policy administration, while others include these costs in the base premium. Compare the actual coverage amounts rather than just the category names, since “full replacement cost” varies between companies. If you call an independent insurance agent, they can quote with multiple companies so you can compare coverage and pricing options. Document each quote’s effective date and expiration terms to avoid gaps in coverage when you switch carriers.

Final Thoughts

Your homeowners insurance comparison demands careful evaluation of coverage types, rate factors, and carrier options. Utah homeowners benefit from below-average premiums at $894 annually, but natural disaster risks require adequate dwelling coverage and specialized endorsements for earthquakes and floods. Independent insurance agents provide access to multiple carriers simultaneously, which streamlines the comparison process and identifies coverage gaps you might miss when you shop alone.

Document your home’s replacement cost, personal property value, and liability needs before you request quotes. Get quotes from at least three carriers with identical coverage limits, then review policy exclusions and available discounts. Consider bundling home and auto insurance for potential savings up to 30% (and evaluate deductible increases that can reduce premiums significantly).

We at Archibald Insurance Agency represent numerous insurance carriers and offer personalized solutions that fit your specific needs and budget. Schedule consultations with independent agents who can quote multiple carriers and explain coverage differences. Your home represents your largest investment, and proper insurance protection requires professional guidance to navigate Utah’s unique risk landscape effectively.